Bond equivalent yield (BEY) is a rate that helps an investor determine the annual yield of a bond (or any other fixed-income security), that does not provide an annual payout. In other words, bond equivalent yield helps an investor find an “equivalent yield” between two or more bonds. It helps an investor to annualize the returns of monthly, quarterly, semi-annual, or other discount bonds to facilitate an apples-to-apples comparison.

Bonds and other such fixed-income securities offer periodic interest payments to investors. These interest payments otherwise referred to as coupon payments, provide a steady stream of income for bond investors.

But there are some types of bonds that pay little or no interest at all to investors. Instead, these bonds are offered to investors at a very deep discount to their par value (face value). Those deep discount bonds that do not offer any interest at all are called zero-coupon bonds since their coupon payment is nil.

In such cases, the investor returns will be the difference between the purchase price of the deep discount or zero-coupon bond and its maturity value. BEY is primarily used to calculate the value of such deep discount or zero-coupon bonds on an annualized basis.

Bond Equivalent Yield Formula

- d = days to maturity

The face value (also known as the par value) of the bond is essentially the price that will be paid to the investor on the maturity of the bond. This will usually be stated on the bond offering.

Also note that, if the bond is coupon-paying, the par value will be the basis for calculating the coupon payments.

The purchase price of the bond is, as the name indicates, the price the investor paid for acquiring the bond. This price will be lesser than the par value in the case of a deep discount or zero-coupon bond.

The number of days until maturity of the bond (d) is essentially is the date on which the par value of the bond will be paid to the investor and is also clearly stated in the bond offering

The BEY formula comprises two parts. The first part calculates the return on investment:

The second part annualizes the return calculated in the first part:

Bond Equivalent Yield Example

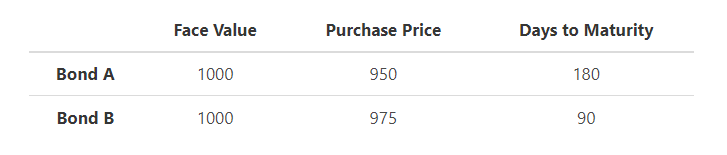

Sam has to choose between investing in the following two bonds:

Which one of the bonds is the better investment option?

Since both of the bonds have the same face value, Sam has to calculate the Bond Equivalent Yield of both the bonds to decide on which would be the better investment option.

First, let’s calculate BEY for Bond A:

Now, Let’s calculate BEY for Bond B:

From the above BEY calculations, it can be concluded that Bond A is a better investment option since its yield of 10.6725% is greater than Bond B’s yield of 10.3989%. Therefore, Sam should invest in Bond A.

Bond Equivalent Yield Analysis

Bond Equivalent Yield is especially useful when an investor has to decide between two or more fixed investment products with different maturities. Since a return is one of the primary criteria for making any investment choice, it becomes essential to compare the rates of return of different investment instruments, despite the difference in payment frequencies.

For instance, if one were to compare a 6-month discount bond with a 12-month bond, other things being equal, in absolute terms, the return from the 6-month bond will be lesser than that of the 12-month one. But, this will not provide a correct view of the real value of the bonds since it does not consider the duration risk for each of the bonds. Generally speaking, the longer the duration, the higher the uncertainty.

The one downside of using the BEY method is that it does not recognize the effect of compounding for shorter duration bonds. In the above example, for instance, in a single year, Bond A could be re-invested only once, (i.e.) after 180 days, during the year. But Bond B can be re-invested three times,(i.e), once every 90 days, during the year. And the re-investment amount would also include the interest earned on the original purchase price. Therefore, the sum received after one year in the case of Bond B could be much higher than Bond A due to the compounding effect.

Let’s explore the compounding effect through another example. Say an investor earns 10% on a semi-annual bond with a face value of $100, then after six months, he would have received an amount of $105 (100+ ((100*(6/12)*10))/100). Now, when he re-invests this sum of $105 for another six months, he would end up receiving $110.25 (105+((105*(6/12)*10))/100). This additional compounding due to the re-investment is ignored in the calculation of bond equivalent yield.

Conclusion

When calculating BEY for an investment the below points are worth bearing in mind as a quick recap of what it is, why it’s used, and how to use it:

- Bond Equivalent Yield helps investors find the equivalent yield between two or more bonds

- BEY is primarily used to calculate the value of the deep discount or zero-coupon bonds on an annualized basis

- Calculation of BEY involves three factors – par value or fair value of the bond, purchase price of the bond, and the time to maturity

- BEY ignores the effect of compounding and therefore might not provide a true and fair picture in certain situations.

Bond Equivalent Yield Calculator

You can use the bond equivalent yield calculator below to quickly calculate and compare bond yield to determine which will give a better return.

FAQs

1. What is the bond equivalent yield?

Bond Equivalent Yield (BEY) is a rate that helps an investor compare two or more fixed investment products with different maturities. BEY takes into account the effect of compounding and helps investors find the equivalent yield between two or more bonds.2. What is the difference between bond equivalent yield and yield to maturity?

The yield to maturity (YTM) is the rate of return that an investor will earn if he holds a bond until its maturity date. The YTM takes into account the effect of compounding.The bond equivalent yield, on the other hand, ignores the effect of compounding and simply provides a rate that helps investors compare two or more fixed investment products with different maturities.

3. What is the purpose of bond equivalent yield?

The bond equivalent yield is primarily used to calculate the value of the deep discount or zero-coupon bonds on an annualized basis. It also helps investors find the equivalent yield between two or more bonds.4. How do you convert the bond equivalent yield to annual effective yield?

The bond equivalent yield can be easily converted to annual effective yield by multiplying it by the number of days in a year. For example, if the bond equivalent yield is 8%, then the annual effective yield would be 8%*365, or 29%.5. How do you calculate the bond equivalent yield?

The calculation of the bond equivalent yield involves three factors – the face value, the purchase price of the bond, and the time to maturity. The BEY is calculated as follows:Bond Equivalent Yield = Face Value−Purchase Price / Purchase Price × 365/d