Why: ClimateSmart.

The high ceiling of climate solutions.

ClimateSmart overweights climate solutions companies because:

They are just at the beginning of their innovation lifecycles (unlike oil).

They have the opportunity to significantly outcompete incumbents, economically.

China has a geopolitical incentive to switch the world to batteries and renewables.

The more of them that get produced, the cheaper (and better) the get.

Chapter 1: Overview

What technology would you rather invest in?

- Horses or cars?

- Newspapers or Search Engine Marketing?

- Blockbuster or Netflix?

The only constant when it comes to technological progress is change. No technology lasts forever, no matter how big, or important to the status quo.

Inevitably, something better, cheaper, faster comes along and replaces it.

At first, the new thing isn’t actually better, cheaper, or faster. It’s more expensive, harder to use, and slower. But the potential is there. If it can escape velocity, avoid getting squashed by the status quo, and get adopted by enough early believers, the process of technological transformation has begun.

The new technology steadily gains adoption. The bigger it gets, the cheaper it becomes. New varieties emerge and social adoption takes off, while the old technology… gets its lunch eaten. Its margins get squeezed as demand drops. The economically weakest parts of the supply chain go out of business, leading to shortages and sudden price hikes. And this messy decline pushes more people to the new solution, faster.

We believe we’re at such an inflection point for multiple climate solutions. And we believe that, simply on their merits (cheaper, better, faster), they are poised to win.

We believe that if we skipped ahead to 2050 and got to ask ourselves that same kind of question: So would you rather have invested in?

- Fossil fuels or solar/batteries?

- Traditional automakers or EV innovators?

That the answer is very clearly the second. And that the same is true for many climate solutions.

Here’s why.

Chapter 2: Renewables and batteries are the cheapest way to generate electricity and prices are still falling

If you wanted to buy something, what would you rather pay $1 or $2?

Would you rather get it tomorrow or the day after?

What if you’re looking to build a new electrical plant?

If you’d prefer the lower price and earlier delivery option, you would no longer go with coal or gas. You’d get a renewables plus battery system.

Don’t take it from us. This is from the March, 2025 presentation from NextEra Energy, one of the largest utilities and energy developers in the US:

Thanks to the falling costs of renewables, solar or wind plus battery storage is now the cheapest way to generate electricity in the US. And thanks to their modular nature, they are also much faster to procure and install than incumbent options like gas. Here’s a graphic from that same presentation:

And this is not just a US phenomenon. In 2022, the International Energy Agency projected that solar plus battery systems would easily outcompete coal in India and China on price:

And that’s coming true. In 2024, China hit a milestone, with their cumulative solar and wind capacity surpassing coal with some analysts estimating that it no longer makes financial sense for China to build more coal capacity.

Why is all of this happening?

For many applications, renewables plus batteries are simply a superior technology for three main reasons:

- They don’t require inputs. You don’t need to worry about the logistics of securing a gas line or supply of coal. You don’t need to factor in accounting for volatile fossil fuel prices. You just need access to wind/sunshine and enough battery backup.

- They are modular. Meaning you can buy enough to power a building or a neighborhood. The base unit (solar panel, battery) is the same.

- Their cost has fallen dramatically. Unlike gas or coal where the main costs are fuel and operating the plant, the main costs for renewables plus storage is just buying and installing the materials. And costs have fallen dramatically as the industry has scaled up:

Solar panels:

Batteries:

Unlike fossil fuels, which get more expensive as the “easy to extract” deposits get exhausted, solar, wind, and batteries are manufactured forms of electricity production.

And humans (particularly the Chinese right now) are really good at optimizing manufacturing. Meaning the more these technologies scale, the cheaper they get. Why? Economies of scale yes, but also just experience. There is a learning curve that as companies build a thing more, they find new efficiencies.

This phenomenon in manufacturing, known as Wright’s Law, projects that every time global capacity doubles for a given manufactured good, prices fall about 20%. We’ve seen that happen for solar and batteries now to the point where they beat incumbents on cost. And, particularly for batteries, there’s no reason to think their advantage won’t just keep growing.

So, it’s no surprise that renewables represented a whopping 93% of electricity expansions in 2024:

And given how much cheaper solar and batteries can still become, it’s hard to see a future for electricity that isn’t moving away from the incumbent coal and gas and towards renewables and batteries.

But what about oil?

Chapter 3: The best cars in the world are Chinese EVs. Watch Out Oil.

It is shocking how quickly the Chinese car market has changed. And it cannot be understated how threatening this rapid evolution is to the status quo of both traditional auto-makers and traditional auto fuel: oil.

Just going back to 2015, Chinese car brands were kind of a joke. Here’s some quotes from an online car enthusiasts forum of that time discussing Chinese cars:

- “Yes they are that bad and not something you want to risk your family in. Look at the crash tests on YouTube and see for yourself.”

- “Not bad as such, but 2 or 3 generations behind. They just copy older cars so if you are happy with a new "old" car then go for it haha... also craftsmanship is not of stellar quality in all cases.”

Jump ahead just 10 years later and the global sentiment has completely flipped. Here’s a selection of headlines:

- Motortrend, 05/21/25: Get In, Losers—China’s Driving the Car-Biz Bus

- European Council on Foreign Relations, 05/15/25: Electric Shock: The Chinese to Europe’s Industrial Heartland

- Jalopnik, 04/15/25: These are the Awesome Chinese Cars You Think America is Missing Out On (this is more of a forum and just shows how far sentiment has come since 2015).

What happened? How did Chinese car companies go from “2 or 3 generations behind” to arguably now “2 or 3 generations ahead?”

First, the Chinese Government, like Elon Musk and the Tesla founders, foresaw that electric vehicles are a fundamentally superior technology to Internal Combustion Engines (ICE). EVs are:

- Cheaper to Manufacture and Maintain: EVs tend to have 25-50 moving parts in their drive trains whereas ICE cars have 200 - 2,000. This unlocks both cheaper costs (it just costs less to manufacture and install 25 things than 2,000) and a lower likelihood of breaking down (moving parts = greater likelihood to break). Also no more oil changes!

- Cheaper to Fuel: According to CNET in 2025, EV drivers can expect to pay an average of $70.72 per month in electricity to “fuel up,” whereas the average IC car driver will pay $152 per month to drive the same distance.

- Faster: Electric cars don’t have gears, meaning they have much faster acceleration than ICE cars. For everyday drivers, this can make getting on the freeway more fun. But EVs also are setting new lap times at famous racetracks.

- Safer: EVs by not carrying around combustible fuels, not needing a big engine in the front, and distributing batteries through the floor have proven to generally be safer than ICE vehicles. In 2023, 60x more ICE cars caught on fire (per 100k cars on the road) than EVs. And their lower center of gravity led to a lower injury rate per crash than ICE.

- More Convenient: If you own a home, you can fuel your car in your garage instead of at the pump.

- More Comfortable: EV engines make far less noise and vibration than an ICE engine, leading to a smoother driving experience. And because the engine and drive train can be distributed across the floor of the vehicle, they can be roomier than ICE cars (although this varies by model).

And second, China under Chairman Xi explicitly stated their goal in their 2021 5-year plan to lead the world in next generation technologies.

And it’s working. In 2025, BYD’s Chairman shared his belief that Chinese “New Energy Vehicles” (aka electric) are ahead of the rest of the world by three to five years.

The numbers back him up. In 2024, BYD surpassed Ford and Honda to become the world’s 4th largest seller of automobiles. They are selling way, way more EVs than American EV leader, Tesla:

So, why is BYD, a Chinese car company that nobody outside of China had heard of 5 years ago, emerging as potentially the #1 car company in the world?

Because unlike Tesla in the US, which enjoyed relatively little competition from other EVs, BYD had to survive and thrive in an extremely crowded, increasingly cutthroat Chinese automobile market.

The New York Times columnist, Thomas Friedman, made the analogy after visiting China in 2025 that Chinese EV companies (and also solar and battery companies) are like athletes all training in the gym against each other. The Chinese government decided that it wanted China to dominate the new electric vehicle industry. It helped fund a bunch of early companies. Each province eventually had a winner they helped support. And those winners entered fierce competition for market share with each other.

The result is that top Chinese EV companies are able to offer much better cars at much lower prices.

The top selling BYD car, the Song, retails for $20k USD in China. For basically the same range and features, you can get its closest US competitor is the Tesla Model Y in the US at a base price of $48k.

That is simply way more car for your money.

And BYD is far from resting on its laurels. In the weeks before writing this article, they announced a major breakthrough in battery technology that checks off another knock against EVs, charging time:

That’s pretty comparable to the time it takes to fill up a gas tank.

And why is BYD working to push ahead technologically so fast? Because CATL, the largest Chinese battery manufacturer, is right on their heals:

Even the CEO of Ford admitted to driving a Chinese EV that comes with features like “air suspension, adaptive dampers, and active aero” and admitted that he “doesn’t want to give it up.” That’s telling.

And while the US tariffs may keep such advanced cars out of US markets, there’s plenty of auto markets out there without domestic production to protect.

Xpeng, yet another successful Chinese EV company, plans to expand its sales from 30 to 60 countries in 2025:

Why are Chinese companies doing so well selling EVs? Why are EVs so popular in what is now the most competitive auto-market in the world (China).

Because EV’s are a better technology. They do everything you like in a car, but better. They are: roomier, safer, quieter, faster, less likely to break down, and cheaper to maintain.

The advantages internal combustion engines still have over EVs are: refueling time and upfront cost. But Chinese companies have basically solved both. And now it’s only a matter of time before such advancements disseminate around the world.

And this doesn’t just stop with passenger vehicles. As they continue to scale battery production Wright’s Law will continue to play out and battery prices will continue to fall. While right now it may not be economically competitive for heavy trucking to use batteries instead of diesel, the economics very well may look different in 5 years.

Meaning it was pretty smart of oil companies to try to squash the electric car in the 90s in the US. (remember that documentary, Who Killed the Electric Car?)

And probably pretty dumb of US automakers allowing Chinese competitors to take the lead.

49% of oil used today is for road transport. That is a big incumbent industry now relying upon an inferior technology somehow holding onto market share.

As long term investors, we know which side of that bet we’d rather be on.

Chapter 4: China has a geopolitical incentive for solar, batteries, and EVs to take over

The 19th century was the “British Century” where the island nation leveraged its early lead on coal power and strong navy to emerge as the global dominant super power.

The 20th was the “American Century” where the country leveraged its manufacturing might and large oil reserves to build its way into major military victories and global dominance of multiple industries.

Now some analysts are wondering whether the 21st century will be the “Chinese Century” as the country leverages its own large population and manufacturing might to take over the industries on the next frontier of technology development.

While we don’t know if China will succeed in replacing America as the pre-eminent global super power, they are not shy about their intentions to do so.

And if they are to follow the same roadmap as Britain and America before them, they will need to emerge as a global leader for not just manufacturing and military might, but also energy.

China’s geopolitical ambitions are a fascinating X-factor for the global fight against climate change. They could end up being the most significant single tailwind accelerating their growth.

A world hooked on renewable energy, batteries, and electric cars is a world where it’s not the fossil fuel exporters who have geopolitical energy dominance anymore, it’s China. The country just has such a significant lead already in these fields. China controls:

- 80% of the solar supply chain (as of 2022)

- 70-80% of the wind supply chain and 100% of critical minerals needed to build wind turbines.

- 80% of global lithium production (for us in EV and energy storage batteries)

- 60% of global EV sales (as of 2023 - likely higher now)

And just like the US does with its domestic fossil fuel industry, the Chinese government has not been shy about massively subsidizing their companies in these spaces to undercut international competition and claim market share.

Are such practices fair?

No.

Is a world of Chinese energy domination a better world?

Probably for our air/water quality and global climate emissions. Unclear for everything else. But it’s not like other global super powers have flexed their energy dominance for the good of humanity (America’s invasion of Iraq)

But China’s momentum in this direction cannot be ignored. While before, solving climate change was a collective action problem, requiring a major shift in global incentives away from profit at all cost to one of embracing shared slowing down and material sacrifice. With China, they are the first major country that could directly benefit materially from addressing climate change in the near term.

So, amidst a backdrop of sharply rising energy demands fueled by AI, the Chinese government has every incentive to make solar panels, batteries, and EVs so good and so cheap that you can’t afford not to use them.

They are well on their way. And barring a global trade alliance against China (which seems very unlikely as of this writing in this post-”Liberation Day” geopolitical climate), there’s not much any individual country can do to stop them.

So what will happen when the cheapest form of electricity on the planet (solar + batteries), being produced by a manufacturing powerhouse with a geopolitical incentive to scale these technologies as fast as possible, encounters the largest sudden increase in demand for electricity since the dawn of air conditioning?

Yep, we need to talk about AI.

Chapter 5: AI’s voracious electricity appetite will scale solar + batteries even faster

Electricity demand is rising around the world.

In developed nations, a period of relatively flat electricity growth has ended as the rise of AI-data centers is projected to increase electricity demand by 20% by 2030.

Whereas in developing and emerging countries, electricity growth is projected to similarly grow, but more driven by a rise in air conditioning and EVs (source: the IEA)

While not all of this electricity demand growth will be met by renewables + battery systems, a lot of it will. They are both cheaper and (importantly for AI) more available.

Let’s start with developed countries and AI.

A hyperscaled data center, the kind that are used to train AI models, can use the same amount of electricity as 100,000 American homes.

In a race against time to get these data centers constructed, tech companies are doing all they can to get these centers through permitting as fast as possible.

And one of the best ways to not strain the grid is to produce electricity on site. That’s a nice boost in demand for renewables.

But it could very well go further, as, for the sake of speed, some tech companies are even looking to ignore the grid altogether. This report outlines why going off-grid can be by far the fastest way to getting a new data center up and running for training AI.

Grid interconnection for such large electricity users can take 5 years. What about just using off-grid gas turbines? You’ll have to wait 3+ years, there’s a major backlog (gas turbines cannot be modularly scaled like solar panels and batteries). But solar plus battery plus a small natural gas backup? That can be done quickly:

Why are we making such a big deal about renewables’ leading role in powering AI?

It comes back to Wright’s Law. Every time the total production for a manufactured good doubles, the price drops 20% as the manufacturers learned a lot about how to improve efficiencies in the process (and more economies of scale don’t hurt either).

The faster more solar panels are built, the faster their price will drop. The faster their price drops, the bigger the delta between their price and fossil fuel options, driving further adoption.

We know the growth trajectory for solar and batteries is up and to the right. The high electricity demands combined with the time pressure for AI hyperscaled data centers to come online simply has the potential to push that growth curve even steeper.

And what about developing countries? As noted above, their electricity demand is also projected to continue rising as they continue to modernize, adding more air conditioning and EVs.

Will this kind of growth be a similar tailwind for renewables and batteries, helping continue their fast march down in price, following Wright’s Law?

Quite possibly.

In multiple frontier markets, those with higher political risk, weaker electrical grids, and high costs of capital, we are seeing a pattern emerge: families and businesses opting to leave the grid for decentralized solar + battery systems.

In Pakistan, sharply escalating electricity prices (to pay back loans to China for financing coal-fired power plants) has led to millions of individual Pakistani households and businesses opting for solar.

In Kenya, solar + battery installations went from 157 MWh in 2023 to 1,641 MWh in 2024, a 10x increase in a year.

In South Africa, a grid plagued with notorious blackouts, solar and battery systems are quickly emerging as the default option for homes and businesses to take their electricity security back under their own control, leading to record growth:

Even in war-torn Lebanon, Hezbollah, the de facto governing political party, offers financing not for diesel generators, but for solar and battery systems. It has worked so well to the point up to 50% of battery stored electricity in off-grid systems isn’t being used. Legislation to allow that power to be sold into the grid is still waiting to be implemented.

All in all, us in the Global North tend to underestimate the Global South. We can unconsciously assume that the pathway developing countries take to modernize will be the same that developed ones did. But the world is changing quickly. It wasn’t economical to use solar and battery systems at scale even just a few years ago. Now, it’s increasingly the economically obvious choice.

The Global South could very much surprise all of us. And that too could be yet another big tailwind driving the growth of renewables, batteries, and EVs.

Chapter 6: Water, heat, and metals: why efficiency climate solutions will win

Remember this?

This was back in 2005. Gas prices had skyrocketed in the US leading to such high demand for the fuel-efficient Toyota Prius, that used ones were being sold above retail prices (because it was very hard to secure a new one).

While the early adopters of the Prius were largely environmentally motivated, the next wave came for a different reason: efficiency.

Efficiency is simply the act of doing more with less. To put it in business-terms, it’s using Capital Expense (CapEx), i.e. a lump sum now, to reduce Operational Expense (OpEx), how much you pay each month to run your business.

And when operational expenses surge, it can often, and sometimes quite suddenly be worth it to pay up front and save money over time.

We saw this back in 2005. As gas prices spiked, the OpEx of driving an 80 mile commute to work everyday got wildly more expensive. And so, tens of thousands of individuals did the math and concluded that it was worth it to pay unusually high CapEx prices (used Toyota Prius) to secure a long term reduction in OpEx (much better gas mileage).

And we’ve seen plenty more supply-side shocks since then. Just in the last 5 years alone:

- In 2020 we had the Covid-19 pandemic.

- In 2022, we had the Russian invasion of Ukraine.

- Now in 2025, we have (as of this writing in May), a looming trade war and the ensuing shortages of imported goods.

Cumulatively, all of these events have pushed businesses to fundamentally rethink their supply chains. Whereas before, it didn’t make sense to pay for redundancy, resource efficiency, and/or localized manufacturing, the economics have shifted.

Companies are throwing around terms like “reshoring” and “hardening” supply chains. European groups are looking to insulate themselves from future gas shortages after the supply from Russia got cut off. The days of “just in time” manufacturing may be ending as the imperative switches to reliability and redundancy.

And those three events we referenced are geopolitical in nature. The 2020 - 2025 period could be an exception, and the world of increasing free trade resumes. Or it could be a precursor.

But do you happen to remember what caused the price spike for gas in the US in 2005 (and the ensuing clamor for used Priuses)?

It was Hurricane Katrina.

An extreme weather event caused massive disruptions to the US oil supply chain in the gulf coast. A series of other geopolitical events followed, and Oil had more than doubled in price by 2008:

The unfortunate truth is that as climate change escalates, we are going to see more Hurricane Katrina’s.

Meaning that the supply shocks of the 2020 - 2025 period are more likely to be the new normal than an exception.

So what do companies do in times of shortages? They invest in efficiency.

How can they reliably produce the same output with fewer inputs? How can they source those inputs from more reliable places?

Energy prices spike?

Invest in efficiency. Install high-efficiency heat pumps and long-lasting LED light bulbs. Retrofit with insulation and high-efficiency windows. Install building automation systems that can optimize energy usage.

Water suddenly scarce?

Invest in efficiency. Install leak detection and usage systems to optimize water use.

Overseas metal shortage?

Source recycled metal locally. Given it takes far less energy to recycle metals than make new ones, they could very well be cheaper.

The interesting thing about efficiency climate solutions are their growth curves. They aren’t smooth.

Instead, they are more of a stairway climbing upwards, characterized by periods of slow/flat/stalled growth and then ones of sharp expansion. The key is to stay invested during the flat periods to take advantage of the explosive ones.

Let’s look at what happened to heat pump sales in Europe in 2022.

- Air to water heat pump sales grew by 49%

- Air to air heat pumps grew by 19%

Why? After Russia invaded Ukraine, gas shortages hit the continent as the infrastructure they had been relying upon (Russian pipelines) were shut off.

Since then, global heat pump sales have continued growing, but much more slowly. Natural gas prices have come down and the incentive to hold onto your gas furnace vs. switch is less strong. But it’s only a matter of time until that changes again. Heat pumps are, after all, a superior technology to traditional HVAC systems. While their CapEx is still higher than traditional ones, their OpEx is much lower. And as their popularity grows, Wright’s Law tells us that it’s only a matter of time until heat pumps have reached cost parity with their competitors.

Chapter 7: The wildcard of governmental climate action

And like in our Why Fossil Fuels will Lag article, we leave perhaps the greatest accelerant for climate solutions last: governmental climate action.

As demonstrated above, we believe the growth of most of the climate solutions we invest in is unstoppable.

Renewables, batteries, and EVs are simply better technologies than their fossil fuel competitors. And they are being deployed at scale by a country that has a strong geopolitical incentive to unseat fossil-fuel energy dominance. As such, even if climate change was not occurring, we would expect to continue to see exponential growth for these technologies.

And climate efficiency technologies are, in some ways, a hedge on climate change itself. As climate-induced volatility and disruptions increase, we will see more companies and businesses clamber to invest in greater efficiency and self-reliance.

But we haven’t yet covered another potentially very large tailwind behind climate solutions: government support.

How much more could meaningful government support push up the growth curves for climate solutions?

It could be a major difference.

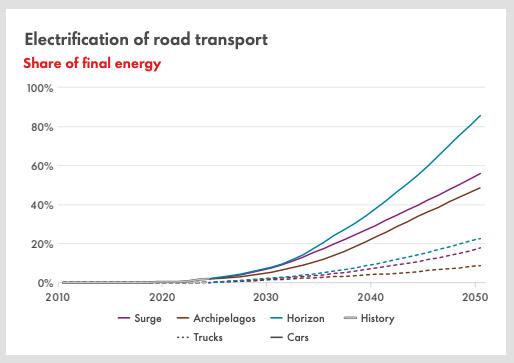

But don’t take our word for it. Let’s again return to that surprising source of optimism for the growth of climate solutions: Shell’s 2025 Energy Security Scenario Report.

In their “Horizon” scenario, they looked at what the results of meaningful global government action to curb global warming could do for climate solutions.

Here’s what they concluded:

Over 80% of the cars on the road are electric by 2050.

And over 80% of the total primary energy the world uses comes from zero carbon sources: renewables and nuclear (which we also invest in).

We hope we see a “Horizon”-like scenario unfold over the coming decades. It not only will mean our investments in climate solution companies do even better, but (much more importantly), that the world has come together to meaningfully address climate change.

But regardless of how the policy landscape unfolds, the growth trajectory of many key climate solutions is just getting started.

FAQ

Frequently asked questions

Could we be wrong?

Absolutely. Nobody can predict the future. Trends that seem to be moving a given direction can change for unforeseen reasons.

We believe the most likely outcome is that climate solutions will be a smart long term bet. The geopolitics, economics, and place on the innovation curb, combined with how the world responds to escalating climate change are powerful drivers. But likely ≠ certain. There are no guarantees when investing.

How do we decide which companies get counted as "climate solution" companies?

We look to the scientists.

Largely drawing from the work at Project Drawdown, we filter the stock market for companies that generate >50% of their revenue from industries that need to scale in the coming decades to mitigate climate change and reduce emissions.

You can see the full list of companies here: https://www.climatesolutionstocks.com/

What happens if governments largely don't take climate action?

Climate change will likely get worse, faster.

But for our portfolios, some less mature climate solutions might grow more slowly than they would have had otherwise. For many of the more mature solutions, however, the takeoff has already begun and we do not believe that much can stop them.

Why aren't we highlighting more exciting climate solutions beyond renewables, batteries, EVs, and efficiency?

The short answer is that, there aren't that many other mature climate solution industries. Exciting companies working on things like geothermal power aren't yet listed on public stock markets for investors like us to put into portfolios.

What about nuclear, a careful reader may ask?

We do invest in nuclear companies, from uranium processors to next generation modular reactor technology companies. Nuclear is a key climate solution.

However, until recently, nuclear had reached somewhat of a stagnant period, or even decline, especially after Fukushima. Now, the bullish investor case for nuclear is two-fold. First, that the universal rise in demand for new electricity for uses like AI will keep older nuclear plants open (or even restart ones that we shut down). Second, that the next generation technologies (both fission and fusion), will make nuclear power both cheaper and more scalable.

While exciting, both of these trends are in much earlier stages than the other trends we highlighted. We are hopeful, but in this piece, we wanted to highlight only actively scaling technologies, not promising "just 5 years away!" ones.

How can I get ClimateSmart in my company's retirement plan?

There's two ways. The easiest is to engage your HR leader to start a conversation with us about becoming your plan's 3(38) advisor. We serve well over 100 organizations and we stand behind how much better we make the 401(k) experience for everyone: leadership, HR, and participants.

But if your company already is working with an advisor they like, another good option is to explore simply adding our ClimateSmart Target Date Fund series to the plan.

Our difference

01.

We're clear eyed.

We think financial security and climate health are directly linked.

02.

We're independent.

We're not owned by a big bank or Wall Street firm.

03.

We're real people.

You'll feel it the moment you meet us.