Inventory to working capital is a liquidity ratio that measures the amount of working capital that is tied up in inventory.

The difference between total current assets and total current liabilities is known as working capital or net working capital. Working capital is the funds that keep the business running daily.

The inventory to working capital ratio allows investors to calculate the exact portion of the business’s working capital that is tied up in its inventories. In other words, inventory to working capital ratio measures how well a company can generate additional cash using its net working capital at its current inventory level. Simply put, inventory to working capital ratio measures the percentage of the company’s net working capital that is financed by its inventory.

This ratio needs to be used in conjunction with other ratios, especially inventory turnover, to make an informed decision. The company might be in an inventory-dependent industry. Also, some companies can have a very high ratio due to financial limitations.

These companies might be more comfortable with a ratio close to 1 in inventory to working capital. The results vary widely across and between industries and companies. Therefore, you should benchmark a company against its industry average.

Inventory to Working Capital Ratio Formula

Working capital is calculated by subtracting current liabilities from current assets. This is represented by combining the accounts receivable and inventories, less accounts payable. This ratio is usually interpreted in terms of percentage. This way, it gives a more realistic picture of the company’s liquidity position.

If the company’s inventory amount is more than other assets, then it can skew the perception of just how readily available a company’s cash truly is for paying off short-term debts. Analysts use this measure in conjunction with other metrics like inventory turnover to make an informed investment decision.

Generally speaking, a lower ratio is desirable as it indicates higher liquidity in a company. A high ratio is an indicator that the company is finding it challenging to convert working capital into cash. This ratio varies; hence it is advisable to benchmark a company’s ratio against the industry’s average.

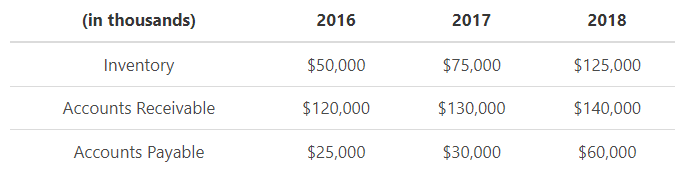

Inventory to Working Capital Ratio Example

ABC Company Limited has gained its competitive edge in the fashion industry in India. The information below has been extracted from the company’s past financial reports.

Use the information in the table above to compute the company’s inventory to working capital ratio in percentage.

Now let’s break it down and identify the values of different variables in the problem for each year. To calculate the net working capital, you would add the accounts receivable and the inventory, then subtract the accounts payable.

Let’s calculate the inventory to working capital ratio for each year:

This example reveals that the company has an increasing trend over time in terms of how its operations depend on the inventory, which is very dangerous. With time it will be challenging for the company to turn over its inventories to make payments to its short term liabilities and accounts payable.

Inventory to Working Capital Ratio Analysis

Liquidity metrics can shed more light on the business’s long term health. By calculating the inventory to working capital ratio, you can understand how much of the working capital is tied to its inventory and how much cash they can generate from the operation. Inventory to working capital measures exactly what portion of the company’s net working capital is funded by its inventories. This ratio is essential to firms who hold stocks and depend on cash supplies to assess the long term viability in terms of fiscal health.

Since this ratio tells us how much of a company’s funds are tied up in inventory for every dollar of working capital, a high ratio implies that nearly all the working capital is tied to its inventory which is very dangerous if they do not sell. Too much inventory in stock attracts storage and maintenance cost, which in turn reduces the company’s profit.

So as an efficiency ratio, firms should ensure that they can know the optimum inventory level to keep to minimize the inventory-related costs such as storage and maintenance. Similarly, if kept for too long, stocks can become outdated hence attracting losses to the firm.

Generally speaking, an increasing inventory to working capital implies that the company is facing an operational problem which may result in difficulties in paying the short-term liabilities and clear the accounts payable. A high ratio in a broad view might mean that inventories are holding more financial strength of the company hence making it very hard for the available working capital to generate any cash. A lower ratio implies that the company can liquidate its inventories very fast and be able to make payments to its current liability. This ratio needs to be done over a long period to watch for trends.

Inventory to Working Capital Ratio Conclusion

- Inventory to working capital ratio is an analytical tool used to accurately calculate the portion of the working capital that is tied to its inventories.

- A high ratio means that the company has an operational problem in liquidating its inventories.

- A low ratio could mean the firm’s operation is efficient in terms of converting its stock inventories into cash hence can generate extra revenue with the available working capital.

- This formula requires two variables: inventories and working capital.

- This should be used in conjunction with the inventory turnover ratio to get an inner picture of the company’s operation.

Inventory to Working Capital Ratio Calculator

You can use the inventory to working capital ratio calculator below to quickly calculate the exact portion of the business’s working capital that is tied up in its inventories by entering the required numbers.

FAQs

1. What is inventory to working capital?

Inventory to working capital is the measurement of how much of a company's working capital is funded by its inventory.

This is an important ratio for any company to monitor as it gives information on the efficiency of its operations. If too much of their working capital is tied up in inventory, then they are unable to pay off short-term liabilities with their available cash.

2. How do you calculate inventory to working capital?

The inventory to working capital is calculated by dividing the total inventory by the total working capital.

The formula looks like this:

Inventory to Working Capital = Inventory / Working Capital

3. What is a good inventory to the working capital ratio?

The ideal inventory to working capital ratio is 1:1.

This means that it takes 1 dollar of inventory to generate 1 dollar of working capital.

If this ratio exceeds between 2:1 and 3:1, then the company has an opportunity for improvement by increasing its turnover rate in order to achieve a leaner operation with less stocked inventories.

4. What impact does inventory have on working capital?

A company's working capital is the amount of money it needs to finance its current operations.

This means that if a firm has too much inventory in stock, then it will have higher expenses and less cash flow available for day-to-day business activities such as payroll and paying bills.

5. Does inventory increase working capital?

No. The amount of inventory held should be equal to the amount of working capital needed.

When this ratio is not balanced, it means that the company has too much stock in its warehouse which results in an increase in operating expenses.