This Basic Financial Statements overview serves as an introduction to financial statements and financial statement concepts. Some of the concepts covered are the accounting equation, double-entry accounting, and debits and credits. Also, two basic financial statements—the balance sheet and the income statement—are introduced.

For more detailed information on financial statements, including statement of cash flows, different types of balance sheets, statement of stockholders’ equity etc, you can explore our library of financial statement articles here.

Overview and Objectives

Financial statements are necessary sources of information about companies for a wide variety of users. Those who use financial statement information include company management teams, investors, creditors, governmental oversight agencies and the Internal Revenue Service.

Users of financial statement information do not necessarily need to know everything about accounting to use the information in basic statements. However, to effectively use financial statement information, it is helpful to know a few simple concepts and to be familiar with some of the fundamental characteristics of basic financial statements.

On completion of this overview, you should be able to:

- Understand the accounting equation

- Know the implications of double-entry accounting

- Distinguish between debits and credits

- Understand what a balance sheet illustrates about a company

- Know how an income statement is put together

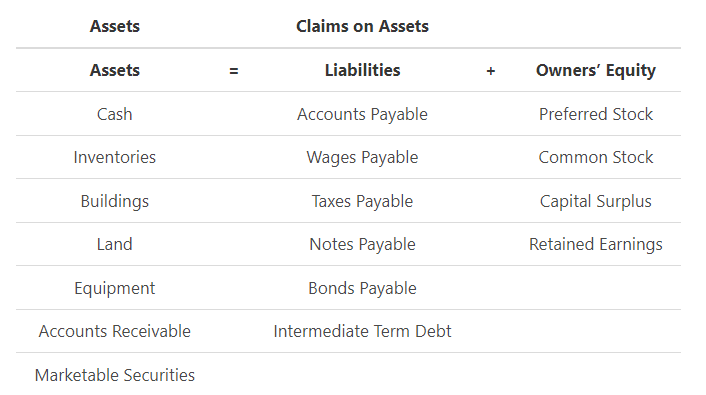

The Accounting Equation

Accounting Equation 1 is an essential notion in financial accounting. The equation derives from assets and claims on assets.

Assets are what a company owns, such as equipment, buildings, and inventory. Claims on assets include liabilities and owners’ equity. Liabilities are what a company owes, such as notes payable, trade accounts payable and bonds. Owner's equity represents the claims of owners against the business.

Assets

- Assets:

What a company owns.

Claims on Assets

- Liabilities:

What a company owes. - Owners’ Equity:

Claims of owners against the business.

The basic equation that expresses the relationship between assets and claims on assets is called the accounting equation:

Some basic assets and claims on assets are listed below.

In other words, the equation illustrates that the assets of the company must equal the claims against the company. Those claims arise from both creditors of the company and owners of the company.

Using the accounting equation, if two of the three components are known, the third can be solved. For instance:

Owners’ Equity must be $150,000 ($200,000 − $50,000).

The Accounting Equation

Double Entry Accounting

For every transaction that is recorded in a business, there have to be two components that make up an entry, a debit, and a credit.

A Debit is:

- An increase in an asset item or

a decrease in a revenue item; - A decrease in a claim item or

an increase in an expense item.

A Credit is:

- An increase in a claim item or

an increase in a revenue item; - A decrease in an asset item or

an increase in a revenue item.

Debits and credits arise whenever a “transaction” occurs, such as a change in assets or a claim on assets.

Assets and Claims on Assets

Debits increase assets or decrease claims on assets (liabilities and owners’ equity). Credits increase claims on assets or decrease assets. To illustrate, consider the following transaction and journal entry reporting the transaction:

A business owner spends cash to purchase a piece of equipment that is to be used in the business. To record this transaction, the owner debits the equipment account because an asset was increased. The offsetting credit would be to cash.

Generally, debits are listed first and credit second. The dollar amount of the debit appears on the left and the dollar amount of the credit appears on the right. If the piece of the equipment illustrated in the transaction above cost $1000, the journal entry to record the transaction would appear as:

Revenues and Expenses

The concept of revenues and expenses is often a little more difficult to understand when first examining the double-entry accounting system. One reason for this difficulty is the fact that revenues are treated as credits while expenses are treated as debits. This concept often seems contrary to the logical notion that revenue means more money; and more money means more assets. The term expenses logically mean a drain on one’s assets. Perhaps when we examine the illustration below, the rationale will seem a little clear.

Recognize, as you examine the illustration, that the assets of a company represent everything that has value, e.g., the cash, the fixtures, the intangibles; everything. These assets are subject to claims by the creditors and the owners. Revenues, however, allow the owners to seek a higher claim in the assets because their profits have increased. Therefore, think of revenues as credits that increase the owner’s equity. Alternatively, expenses are expired assets. They represent contra revenues and reduce the amount of profit to which an owner lays claim.

To illustrate the concept of double-entry accounting related to revenues and expenses, consider an example of a company that sells a service for which the owner charges and receives $300. The journal entry to record the transaction would be:

The cash the owner receives increases the value of the assets, while the revenue account allows the owner to increase his claim against those assets.

Now suppose that in order to earn that $300 in the above example, the company incurred a utility bill of $100. As the company writes a check, it will make the following journal entry:

In this example, the company has exhausted $100 (an expired asset) and it reduces cash accordingly. The expense is reflected as a contra revenue and reduces the owner's claim against the remaining assets of the company. Note that if the utility bill had not been paid, the credit would not reduce cash (the assets have not yet been exhausted), instead, the credit would have gone to a liability (showing that the creditors have a claim of $100 against the company’s assets).

To review, the following table shows what might be considered debits and credits.

Debit:

- Increases in Assets

- Decreases in Claims

- Expense Items

Credit:

- Decreases in Assets

- Increases in Claims

- Revenue Items

Double Entry Accounting and The Accounting Equation

In double-entry accounting, for every debit, there must be an offsetting credit. One helpful tool for understanding debits and credits might be to think in terms of the left and right sides of the accounting equation. The left side represents the assets of the company and the right side represents the claims on those assets; i.e., liabilities and owners’ equity. Generally, anything that increases the left side or decreases the right side would be considered a debit and anything that increases the right side or decreases the left would be considered a credit.

As previously illustrated, revenues and expenses may also be thought of in terms of the accounting equation. Since owners’ equity is a claim on assets, it would therefore fall on the right-hand side of the equation. Revenues would be considered credits because, in essence, they would eventually tend to increase ownership in the business. Expenses would take away from the ownership and so they would fall on the left-hand side of the equation.

Debits and Credits, and the Left–Right Notion

This “left–right” notion carries through into journal entries where the debit is recorded on the left side of the transaction and credits are recorded on the right. An example of this “left–right” thinking may be constructed using an example where a $500 materials expense that was charged on a trade account is to be recorded. The expense would eventually decrease ownership in the company when it is paid. It therefore would impact on the left side of the accounting equation, so it would be a debit.

The charging of the materials would be an increase in liability (accounts payable). That increases the claims on the company, so it would be considered a credit. The journal entry to record this transaction would be:

Note that the debit appears first and the dollar amount appears on the left side of the journal entry. The credit is listed second and appears on the right-hand side.

The Balance Sheet

The Balance Sheet is a statement detailing what a company owns (assets) and claims against the company (liabilities and owners’ equity) on a particular date. Some analysts liken the balance sheet to a snapshot illustrating a company’s financial health.

Keeping in mind the assets and claims, it is helpful to remember the “left–right” accounting equation orientation; assets on the left side, claims on the right. In addition, there are a number of other characteristics of the balance sheet that are noteworthy, such as balancing, order of listing, valuing of items, and definitions of items. These items are discussed with an example balance sheet to illustrate the points.

Balancing the Balance Sheet

The balance sheet must balance; that’s why it’s called a balance sheet. In other words, the assets must equal the claims on assets. The concept of balancing relies on the accounting equation which was discussed earlier in this lesson.

Order of Listing

Items on a balance sheet are listed in order of liquidity2. Liquidity takes on a slightly different meaning for assets and for claims on assets. For assets, liquidity means nearness to cash. For this reason, cash is the first item on the balance sheet.

After cash, the other current assets are listed in order of liquidity. Marketable securities (which can be converted to cash by selling them), accounts receivable (which may be factored), and finally, inventories make up the rest of the current assets. Inventories, which are considered current assets, are listed last because it is generally harder to convert to cash a half-finished item in production than it would a U.S. Treasury bond, for example.

Following current assets come those assets that would take more time to convert to cash. Buildings, land, and equipment would all be considered long-term or fixed assets3.

When ranking claims on assets, liquidity refers to how quickly the claim against the company matures. Short-term or current liabilities mature quickly. Intermediate, and then long-term liabilities would be listed next. Sometimes as longer-term liabilities move toward maturity, the portion that matures is moved into current liabilities.

Last on the claims portion of the balance sheet would be the equity accounts. For a corporation, the preferred stock accounts would be listed before common equity accounts. The last claimants on a company’s assets are the common stockholders.

Valuing Balance Sheet Items

Items on the assets side of the balance sheet are generally valued at cost. There are two exceptions—marketable securities and inventories. The rule that applies to marketable securities and inventories is lower of cost or market. That means that current market value or original cost, whichever is lower, is the appropriate value for marketable securities and inventories. For instance, if a share of stock was originally purchased for $80 three years ago and its value has fallen to $60, the value that would appear on the balance sheet is $60.

One note that should be made is in reference to accumulated depreciation. The accumulated depreciation account is what is called a contra-asset4 account. That means that even though accumulated depreciation is reflected on the assets portion of the balance sheet, it in essence carries a minus sign. Therefore, if Gross Fixed Assets are $1,000,000 and Accumulated Depreciation is $200,000, Net Fixed Assets would be $800,000.

Definitions of Balance Sheet Items – Assets

Balance sheets may be quite detailed depending on the nature and complexity of a business. Regardless of their complexity, however, the same basic notions of construction apply. Again it is helpful to keep in mind the “left–right” balance sheet orientation. An illustration of a somewhat complex balance sheet may help understand the different types of accounts. Assets5 will be covered first on this page, and then claims on assets will follow.

| Assets | ||

|---|---|---|

| Current Assets6 | ||

| Cash7 | $50,000 | |

| Marketable Securities8 | $70,000 | |

| Accounts Receivable9 | $95,000 | |

| Notes Receivable10 | $50,000 | |

| Inventories11 | $90,000 | |

| Total Current Assets | $355,000 | |

| Long-Term Assets12 | ||

| Tangible Assets13 | ||

| Land14 | $89,000 | |

| Buildings15 | $99,000 | |

| Machinery16 | $35,000 | |

| −Accumulated Depreciation17 | −$5,000 | |

| Net Tangible Assets18 | $218,000 | |

| Intangible Assets19 | ||

| Goodwill20 | $20,000 | |

| Patents21 | $19,000 | |

| Trademarks22 | $13,400 | |

| Organizational Costs23 | $22,900 | |

| Total Intangible Assets | $75,300 | |

| Other Assets24 | ||

| Investments25 | $23,000 | |

| Deferred Charges26 | $53,000 | |

| Total Other Assets | $76,000 | |

| Total Long-Term Assets | $369,300 | |

| Total Assets | $724,300 |

Definitions of Balance Sheet Items – Claims on Assets

Claims on assets arise from debt and from ownership claims on the company. As the number of liabilities and ownership items increase, the complexity of the balance sheet increases.

| Claims on Assets | ||

|---|---|---|

| Liabilities27 | ||

| Current Liabilities28 | $18,000 | |

| Notes Payable29 | $39,000 | |

| Accounts Payable30 | $15,000 | |

| Taxes Payable31 | $13,000 | |

| Accrued Expenses32 | $43,000 | |

| Other Current Liabilities33 | $11,000 | |

| Total Current Liabilities | $139,000 | |

| Long-Term Liabilities34 | ||

| Notes Payable35 | $18,000 | |

| Bonds Payable36 | $99,000 | |

| Total Long-Term Liabilities | $117,000 | |

| Other Liabilities37 | ||

| Pension Obligations38 | $98,900 | |

| Deferred Taxes39 | $72,000 | |

| Minority Interest40 | $12,400 | |

| Total Other Liabilities | $183,300 | |

| Total Liabilities | $439,300 | |

| Owners Equity | ||

| Preferred Stock41 | $12,000 | |

| Common Equity42 | ||

| Common Stock43 | $118,000 | |

| Capital Surplus44 | $110,000 | |

| Retained Earnings45 | $100,000 | |

| −Treasury Stock46 | −$55,000 | |

| Total Common Equity | $273,000 | |

| Total Owners’ Equity | $285,000 | |

| Total Claims on Assets | $724,300 |

The Income Statement

The Income Statement47 shows a firm’s revenues and expenses, and taxes associated with those expenses for some financial period. Where the balance sheet may be thought of in terms of the “left–right” orientation previously discussed, the income statement would be thought of in “top–down” terms.

A basic overview of income statement items shows how a manufacturing company might present an income statement. Income statements for other companies may appear to be slightly different, but in general the construction would be the same.

An important concept in understanding the income statement is Earnings Per Share (EPS). The EPS for a company is net income divided by the number of shares of common stock outstanding. It represents the bottom line for a company.

Companies continually make decisions on how their bottom line will be impacted since shareholders in the company are concerned with how management decisions affect individual shareholder position.

| 48 | Sales 125,000 units @$125 each | $ 15,625,000 |

| − Cost of Goods Sold | − 10,000,000 | |

| 49 | Gross Profit | 5,625,000 |

| − Selling, General, Administrative Costs | − 2,350,000 | |

| 50 | Operating Income Before Depreciation | 3,275,000 |

| − Depreciation, Amortization, Depletion | − 10,500 | |

| 51 | Operating Profit | 3,264,500 |

| − Interest Expense | − 90,000 | |

| 52 | Non operating Income | 40,000 |

| − Non operating Expenses | − 50,000 | |

| 53 | Pretax Accounting Income | 3,164,500 |

| − Income Taxes | − 1,550,000 | |

| 54 | Income Before Extraordinary Items | 1,614,500 |

| − Preferred Stock Dividends | − 90,000 | |

| 55 | Adjusted Net Income | $ 1,004,500 |

| 56 | Earnings Per Share (900,000 shares of stock) | $ 1.12 |

In studying financial statements, it is helpful to remember that they are only a tool to be used by different entities. For the purposes of this overview, the perspective is that of a manager. Think about the kinds of information managers need to have in order to make effective decisions and how that information might be used.

The balance sheet and income statement are both basic statements common to most businesses. Another group of statements are based on the concept of how funds flow through a business. Two such statements are the statement of retained earnings and the statement of cash flows.

To learn more about the uses of these financial statements, review the Ratio Analysis Overview which covers the notion of funds flow and the statement of retained earnings and the statement of cash flows.

This overview was developed by Dr. Sharon Garrison.

No adaptation of its content is permitted without permission.

-

Assets = Liabilities + Owners’ Equity↩

-

For assets, liquidity is nearest to cash. For liabilities, liquidity refers to how quickly the claim will mature.↩

-

Long-term assets.↩

-

An asset item which would in essence carry a minus sign.↩

-

Rights or resources that have future benefit or service potential, which can be expressed in money terms and which result from a business transaction.↩

-

Liquid assets↩

-

Negotiable checks and checking account balances, cash on hand. Savings accounts are usually classified as cash.↩

-

Ownership and debt instruments that can be readily converted to cash.↩

-

Monies due on accounts from customers.↩

-

Monies due from debtors.↩

-

Balances of goods on hand. Include raw materials, work in process, finished goods.↩

-

Generally, long-term assets take longer than a year to be converted to cash.↩

-

Physical facilities used in the operations of the business.↩

-

Shown at acquisition cost and not depreciated.↩

-

Structures valued at cost plus permanent improvements.↩

-

Equipment listed at historical cost.↩

-

Contra-asset account. Reduces gross fixed assets.↩

-

Gross tangible assets minus accumulated depreciation.↩

-

Nonphysical assets such as legal rights or excess earning power caused by a business transaction.↩

-

Arises from the acquisition of a business for a sum greater than physical asset value.↩

-

Exclusive legal rights granted to an investor for a period of 17 years.↩

-

Distinctive names or symbols. Granted for 28 years with option for renewal.↩

-

Legal costs incurred when a business is organized. Carried as an asset and usually written off over a period of 5 years or longer.↩

-

Assets that do not fit into one of the other classifications.↩

-

Usually stocks and bonds; as well as monies set aside in special funds.↩

-

Expenses which have been deferred until some future period.↩

-

Debts owned by an entity that can be satisfied through disbursing assets or rendering services.↩

-

Those that require meeting the obligation within one year.[]/footnote] Long-term Debt : 1 Yr.[footnote]That portion of long-term debt which is maturing within the year.↩

-

Debt owed on a short-term note.↩

-

Short-term obligations, created by the acquisition of goods and services.↩

-

Taxes due within the year.↩

-

Short-term obligations, such as salaries, for services received but not yet paid.↩

-

As an example, dividends payable. Those items that do not fit into other categories.↩

-

Due in period exceeding one year.↩

-

Promissory notes.↩

-

Obligation due on maturity value of bonds.↩

-

Liabilities relating to operational obligations such as pension obligations, deferred taxes, service warranties.↩

-

Liabilities for future pension benefits due employees.↩

-

Longer-term tax obligations which have been deferred to some future period.↩

-

Ownership of minority shareholders in the equity of consolidated subsidiaries. Generally considered a liability. (It is usually seldom material.)↩

-

Special class of stock.↩

-

Ownership of common stockholders. Common stock, capital surplus and retained earnings.↩

-

Number of shares outstanding times par value.↩

-

Reflection of amount received per share of stock in excess of par value.↩

-

Undistributed earnings of the corporation.↩

-

Stock in the company which has been repurchased and not retired.↩

-

A statement showing a firms revenues, and costs and taxes associated with those revenues for some financial period.↩

-

Sales: Selling price of product × number of products sold.

Cost of Goods Sold: Materials and labor expenses for products sold.↩ -

Gross Profit: Sales minus cost of goods sold.

Selling, General, Administrative Costs: Items such as rent, executive salaries, sales commissions.↩ -

Operating Income Before Depreciation :Gross profits minus selling, general and administrative costs.

Depreciation, Amortization, Depletion: Noncash expenses reflecting decline in asset value.↩ -

Operating Profit: Operating income before depreciation minus depreciation.

Interest Expense: Financial expenses on borrowed funds for current income period.↩ -

Non operating Income: Income arising from sources other than primary operations. For instance, a manufacturing company’s dividend income on investments.

Non operating Expenses: Expenses arising from sources other than primary operation.↩ -

Pretax Income: Operating profits minus interest and non-operating expenses plus non-operating income.

Income Taxes: Tax expense on income for current income period.↩ -

Income Before Extraordinary Items: Pretax income minus income taxes.↩

-

Income Available for Common Stockholders: Income before extraordinary items less preferred dividends.

Extraordinary Items: Items that do not arise in the ordinary course of business. Must be unusual and occur infrequently. An example might be loss from a hurricane.

Discontinued Operations: Writing off of a discontinued line of business.[footnote]Income Available for Common Stockholders1,524,500− Extraordinary Items

− Discontinued Operations− 20,000

− 500,000[footnote]Adjusted Net Income: Income Available for Common Stockholders minus Extraordinary Items and Discontinued Operations. The final result for the current financial period for a company. Out of this figure common stock dividends will be paid and the remainder will be shown as a transfer to retained earnings.↩ -

Earnings Per Share: Adjusted Net Income divided by the Number of Shares of Stock Outstanding.↩

FAQs

1. What are financial statements?

Financial statements are a company’s record of its financial performance over a specific period. The most common financial statements are the income statement, balance sheet, and cash flow statement.

2. What are the different types of financial statements?

The three most common financial statements are the income statement, balance sheet, and cash flow statement.

3. What are the components of financial statements?

The three most common financial statements are the income statement, balance sheet, and cash flow statement. The components of each statement vary depending on the type of statement. However, all three statements typically have revenue, expenses, assets, and liabilities.

4. What is the importance of financial statements?

Financial statements are important because they provide a snapshot of a company’s financial performance. They can be used to assess a company’s financial health, track trends, and make comparisons to other companies. Financial statements are also used by investors, lenders, and other interested parties to make decisions about the company.

5. What are the characteristics of financial statements?

Financial statements are typically in a standard format, have standard terminology, and are audited. Financial statements should also be able to stand alone and be understandable without additional explanations.