Free Cash Flow to Equity (FCFE) is a valuation metric that determines the amount of cash that is potentially available to equity shareholders after all the expenses of the company have been taken care of. Put simply, it is the amount of cash that the company generates after meeting various obligations such as capital expenditure, re-investment, debt, and other expense obligations.

Free Cash Flow to Equity Formula

.png?width=598&name=Screenshot%20(50).png)

- Cash from Operations can be found in the Cash Flow statement under the “Cash from Operations” section

- Capital Expenditure can also be found in the Cash Flow statement under the “Cash from Investing” section

- Net borrowing can be calculated by subtracting the amount of debt repaid in the year from the total debt borrowed during the year. Both these figures can also be found in the Cash Flow statement under the “Cash from Investing” section.

From Net Income

The formula for FCFE can be rewritten as follows:

This is because:

- Net Income can be found at the bottom of the income statement

- Depreciation and amortization and other non-cash expenses can also be found on the income statement under the “Expenses” section

- Changes in Working capital are the net of current assets and current liabilities. Therefore, it could be either positive or negative. If changes in working capital are positive, add that amount else subtract it from the net figure.

- Current Assets are usually inventory and receivables while Current liabilities are payables and other accrued liabilities and all of them are listed in the balance sheet under the Current Assets and Current liabilities section respectively

- Net borrowings is the net of debt issued and debt repaid during the year and therefore can be both positive or negative. Debt includes both long-term and short-term debt and can be found in the balance sheet under the Liabilities section

From Earnings before Income and Tax (EBIT)

We know that:

We also know that:

.png?width=289&name=Screenshot%20(56).png)

This means we can also rewrite the formula as:

EBIT can be found in the company’s income statement and both Interest and taxes will also be listed in the income statement below EBIT.

From Earnings before Interest, Taxes, Depreciation, and Amortization (EBITDA)

EBITDA provides a better measure of the operating profitability of the company since it excludes depreciation and amortization expenses. We know that net income can be calculated using EBITDA through the following formula:

.png?width=536&name=Screenshot%20(57).png)

Substituting the above equation for net income in the FCFE formula, we get:

This can be rewritten as:

EBITDA can also be found in the income statement of the company.

Free Cash Flow to Equity Example

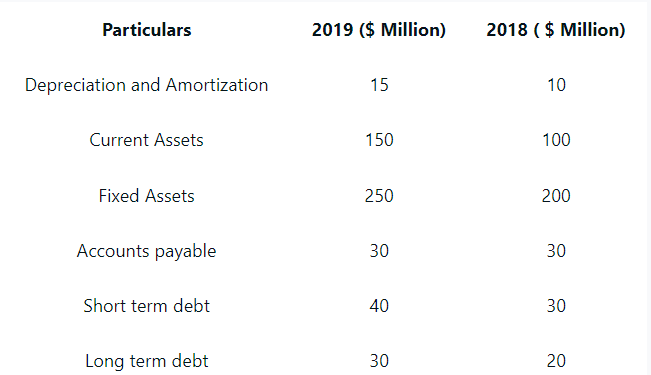

You have been provided with the following details from Company A’s Balance Sheet and Income statement:

The company’s net income for the year 2019 is $200 million. Find out the free cash flow to equity of the firm.

Since net income has been provided to us, let’s solve for FCFE using the formula:

.png?width=308&name=Screenshot%20(62).png)

- Net Income is $200m

- Depreciation & Amortization for 2019 is $15m

- Let’s now calculate the changes in Working Capital

- Difference in Current Assets = 100-150 = -50

- Difference in Current Liabilities = 30-30 = 0

- Therefore, change in working capital would be (-50-0) = -50

- Change in Capital Expenditure would be equal to 250-200 = 50

- Net borrowings would be the total of short term and long term debt

- Difference in short term debt = 40-30 =10

- Difference in long term debt = 30-20 = 10

- Net Borrowings = Short term Debt+Long term Debt = 10+10 = 20

From this we can see that company A has a positive FCFE of $135m which is potentially available for equity shareholders.

Free Cash Flow to Equity Analysis

Free Cash Flow to Equity is an alternative to the Dividend Discount Model for estimating the value of a firm under the Discounted Cash Flow (DCF) valuation model. The dividend Discount Model of valuation can be used only when a firm maintains a regular discount payout. But there are multiple companies that do not pay dividends regularly. Some of them despite being profitable does not pay dividends. Instead, they might reinvest the excess cash generated, back in the business either to sustain or increase the growth rate of the company. In such cases, it is impossible to value the company based on the Dividend Discount Model (DDM). Another disadvantage of using the DDM is that dividends paid by the company might not exactly reflect the true picture of the business capacity of the company.

FCFE was developed as an alternative to estimate the value of a firm since it uses equity as the basis for firm valuation. It is especially useful for calculating the value of a firm that pays little or no dividends. Using the FCFE, you can find out the Net Present Value of the company’s equity. Under the DCF model, this can be done by discounting the FCFE at the required rate of return on equity. We can now use this equity value to calculate the theoretical share price of the firm.

FCFE can also be used to find out if the firm is paying for stock buybacks and dividends using free cash flow available to equity holders or whether it is using debt to finance them. If the FCFE is less than the cost of dividend payments and stock buybacks, one can conclude that the company is using debt to finance the payments. Another possibility is that the company is issuing new shares or is using retained earnings of previous years to fund the same. You can find that out by noticing the difference in Share Capital and/or retained earnings between the current financial year and the previous financial year.

Conclusion

To sum up:

- FCFE is used to determine the amount of cash that is potentially available to the equity shareholders of a company after meeting all its debt, re-investment, and expense obligations.

- FCFE is an alternative to the Dividend Discount Model for calculating the fair value of the stock of a company.

- FCFE is used to calculate the equity value of a firm under the DCF model, especially when the firm pays little or no dividends.

- FCFE can be used to find out if a firm is using debt to finance its stock repurchases or dividend payments

Free Cash Flow to Equity Calculator

You can use the free cash flow to equity calculator below to easily find the amount of cash that is available to equity shareholders after expenses by entering the required numbers.

FAQs

1. What is free cash flow to equity?

Free cash flow to equity (FCFE) is the cash generated by a company that is available to be paid to its equity shareholders after meeting all of its debt and reinvestment obligations. This is an important metric for estimating a company's value under the discounted cash flow (DCF) valuation model.

2. What is the formula of free cash flow to equity?

The formula for FCFE is: FCFE = Cash from Operations − Capital Expenditure (Capex) + Net Borrowing

- Cash from Operations can be found in the Cash Flow statement under the “Cash from Operations” section

- Capital Expenditure can also be found in the Cash Flow statement under the “Cash from Investing” section

- Net borrowing can be calculated by subtracting the amount of debt repaid in the year from the total debt borrowed during the year. Both these figures can also be found in the Cash Flow statement under the “Cash from Investing” section.

3. Is Free Cash Flow (FCF) the same as FCFE?

No, FCF is not the same as FCFE. Free cash flow (FCF) is the total cash generated by a company, including cash from operating activities, investing activities, and financing activities. However, FCFE only includes the cash generated by operations and investing activities (excluding financing activities). This is because the net borrowing used to calculate FCFE is the amount of debt that was repaid during the year, which is a financing activity.

4. When should a company use the free cash flow?

A company should use free cash flow when it wants to assess its ability to pay dividends, repurchase shares, or service debt. FCFE can also be used to estimate the value of a company under the discounted cash flow model.

5. What is an example of a free cash flow to equity?

An example of FCFE would be a company that generated $100 million in cash from operations, spent $50 million on capital Expenditures, and had net borrowing of $10 million. In this case, the FCFE would be $40 million ($100 million − $50 million + $10 million).