Closing entries are manual journal entries at the end of an accounting cycle to close out all the temporary accounts and shift their balances to permanent accounts. In other words, temporary accounts are reset for the recording of transactions for the next accounting period. By doing so, companies move the temporary account balances to the permanent accounts of the balance sheet.

The Accounting Cycle Example

Throughout this series on the accounting cycle, we will look at an example business, Bob’s Donut Shoppe, Inc., to help understand the concepts of each part of the accounting cycle. Below is the complete list of accounting cycle tutorials:

- Journal Entries

- T-Accounts

- Unadjusted Trial Balance

- Adjusting Entries

- Adjusted Trial Balance

- Preparing Financial Statements

- Accounting Worksheet

- Closing Entries (you are here)

- Income Summary Account

- Post-Closing Trial Balance

- Reversing Entries

We also have an accompanying spreadsheet which shows you an example of each step.

Click here to download the Accounting Cycle template

Temporary Accounts

These are general account ledgers that record transactions over the period and accounting cycle. These account balances are ultimately used to prepare the income statement at the end of the fiscal year. Examples of temporary accounts include revenue, expense and dividends paid accounts.

A temporary account records balances for a single accounting period, whereas a permanent account stores balances over multiple periods. For instance, the year 2020 revenue and expense accounts would show the balances pertaining to just that year and not for 2019 or 2018.

Permanent Accounts

These are general account ledgers that show balances recorded over multiple periods. These will usually include all balance sheet items like assets, liabilities and equity accounts. Therefore, all those accounts are included for which current balances must be used in the next financial reporting period and for which accounts cannot be closed out. They track activities lasting more than one accounting period.

Preparing Closing Entries

There are two ways to close a temporary account. It can directly be closed in the retained earnings account or it can be done through a longer process. The longer process requires temporary accounts to be closed in an intermediate income summary account first and then that account is zeroed out to the retained earnings. The result in both cases is the same and depends on the bookkeeper’s preference or company’s policy on it.

Both methods are correct with each having its advantages and disadvantages. The direct method is faster and less complicated as there is no intermediate account involved and requires ones less step. The method of first moving the balances to an income summary account and then shifting the balances to the retained earnings account will be more time consuming for the company. However, it will provide a better audit trail for the accountants who review these at a later point in time.

The accountant can choose either method as eventually all the accounts will be transferred to the retained earnings account on the balance sheet.

Income Summary Account

As mentioned earlier, this is just an intermediate account that is used to zero out all the other revenues and expenses accounts into one place. The balances of the income summary account will eventually also be transferred to the retained earnings account on the balance sheet.

Examples of Closing Entries

Below are some of the examples of closing entries that can be used to transfer revenue and expense account balances into income summary and from there to the retained earnings.

Close Revenue Accounts

To close the account, we need to debit the revenue account and credit the income summary account. This will ensure that the balances of the revenue account are transferred to the income summary account.

Close Expense Accounts

To close the account, we need to debit the income summary account and credit all the relevant individual expenses accounts such as utilities expense, wages expense depreciation expense, etc. This will ensure that the balances of those expenses account are transferred to the income summary account.

Close Income Summary

To close the income summary account to the retained earnings account as mentioned earlier, we need to debit the income summary account and credit retained earnings account. This will ensure that the balance has been transferred on the balance sheet.

Close Dividends Account

The last account to close is the dividend account. Here we need to debit retained earnings account and credit dividends account.

Bob’s Donut Shoppe Example

As we have prepared Bob’s accounting worksheet in the previous step, it’s now time for the closing entries for Bob’s financial year-end. These will look something like these:

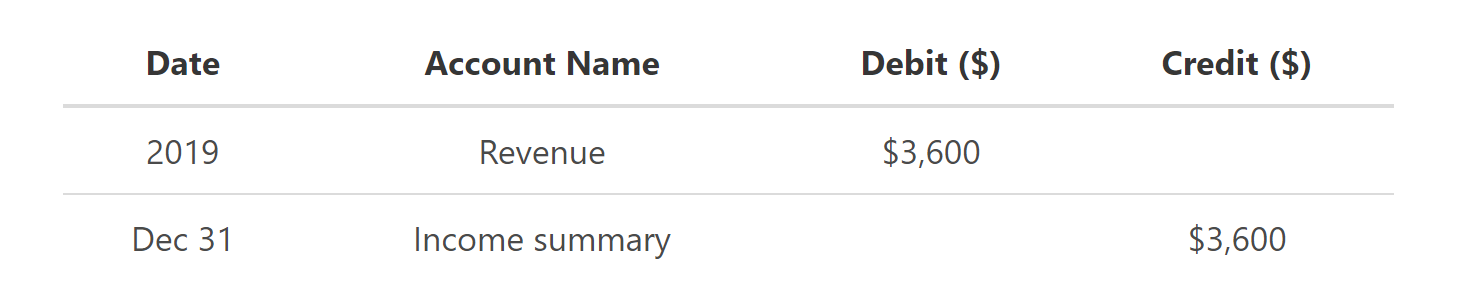

Closing Entry #1 for Bob

To close the revenue accounts for Bob’s Donut Shoppe, we need to debit the revenue account and credit the income summary account. This will ensure that the balances of the revenue account are transferred to the income summary account.

From the above entry, we can see that Bob had made $3,600 in revenue for January 2020.

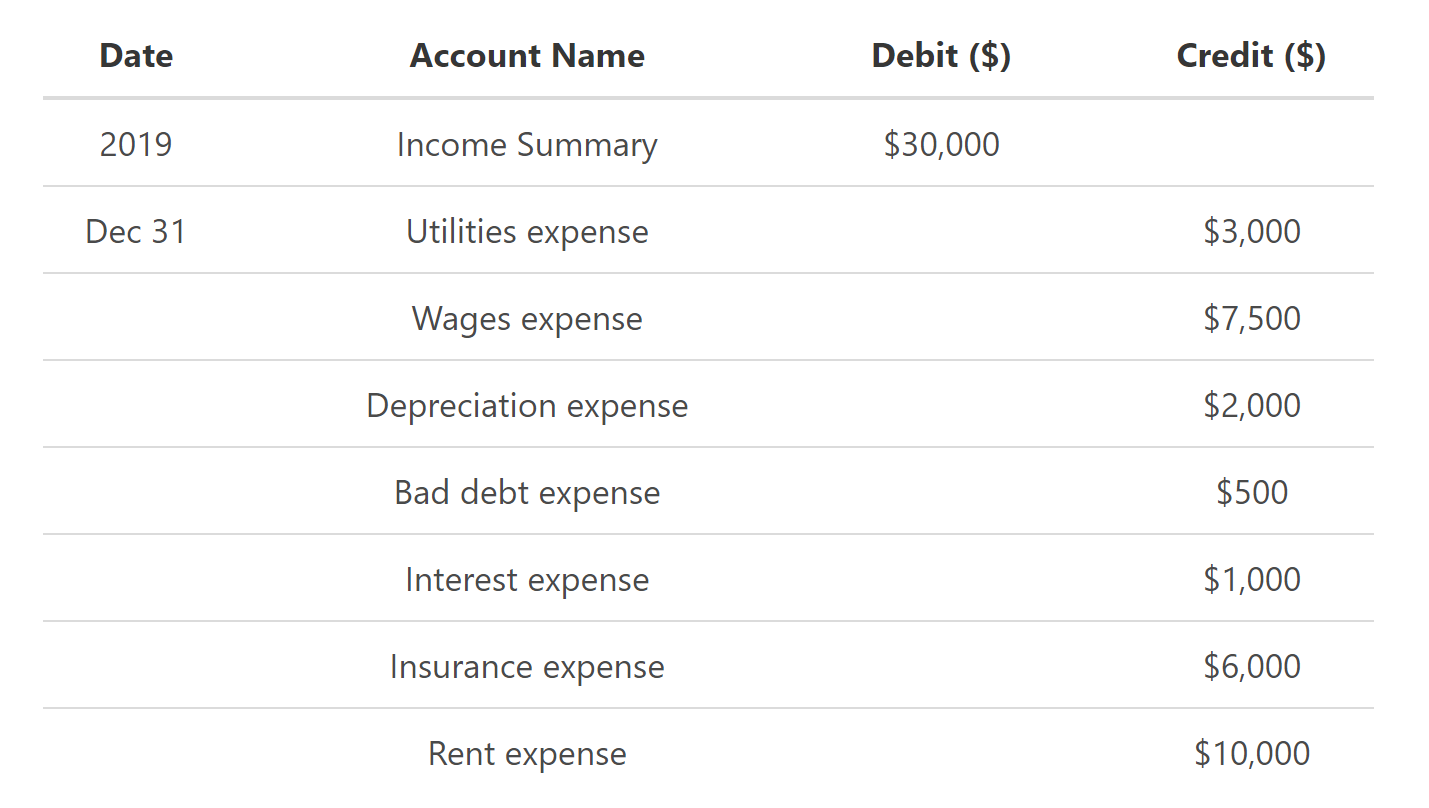

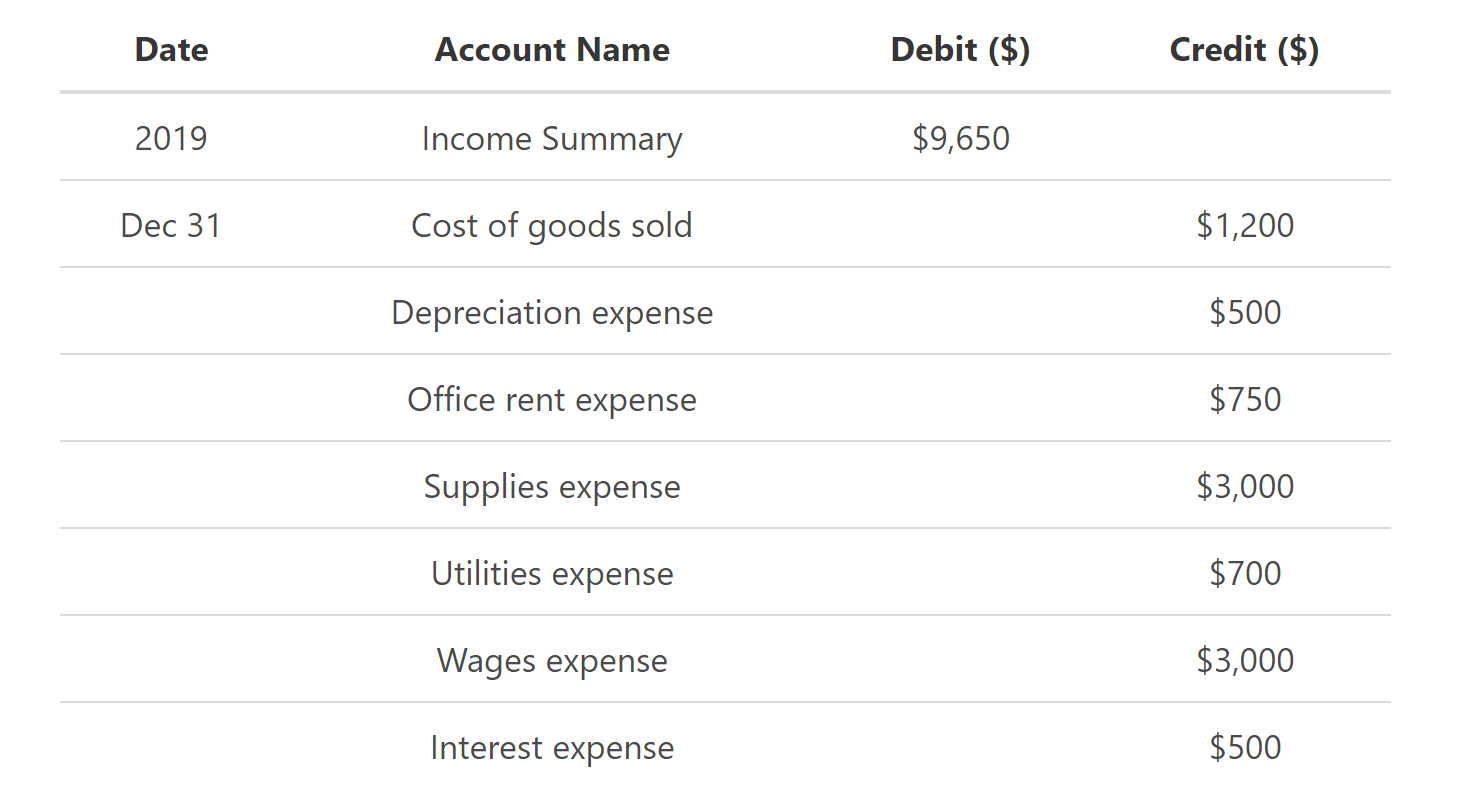

Closing Entry #2 for Bob

To close the expense accounts for Bob, we need to debit the income summary account and credit all the relevant individual expenses accounts such as utilities expense, wages expense depreciation expense, etc. This will ensure that the balances of those expenses account are transferred to the income summary account.

Here we see that total expenses for both were $9,650 for January 2020.

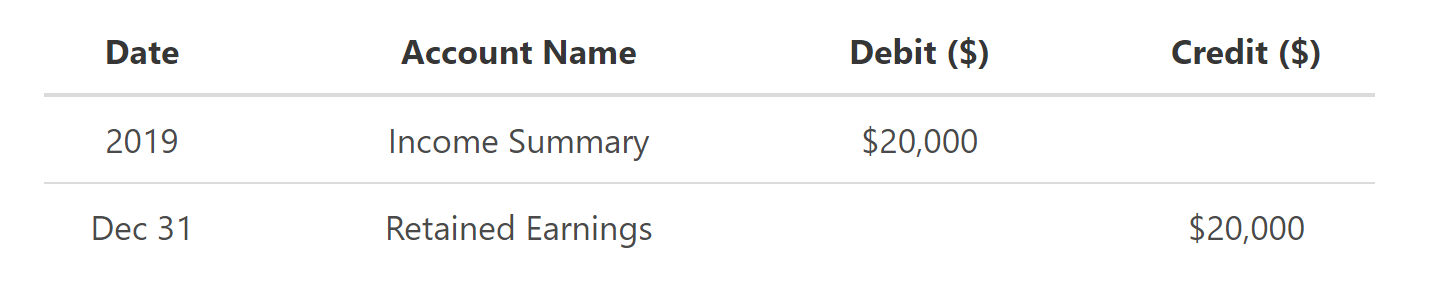

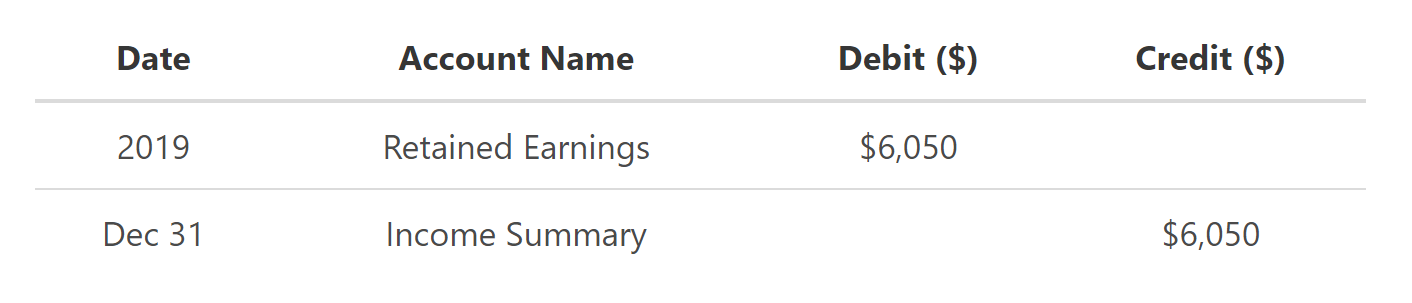

Closing Entry #3 for Bob

To close the income summary account to the retained earnings account, Bob needs to debit the retained earnings and credit the income summary. This is contrary to what is normally done, as Bob has made a net loss for the period. Therefore, this entry will ensure that the balance has been transferred on the balance sheet.

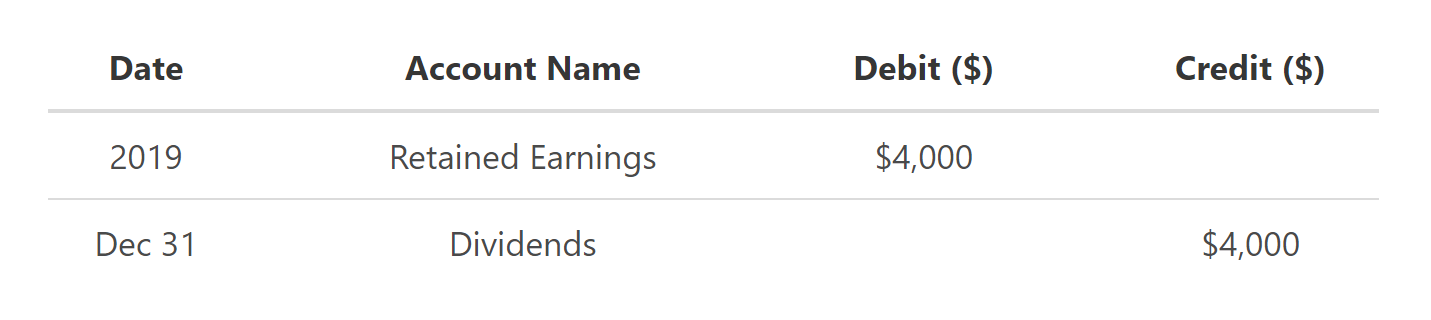

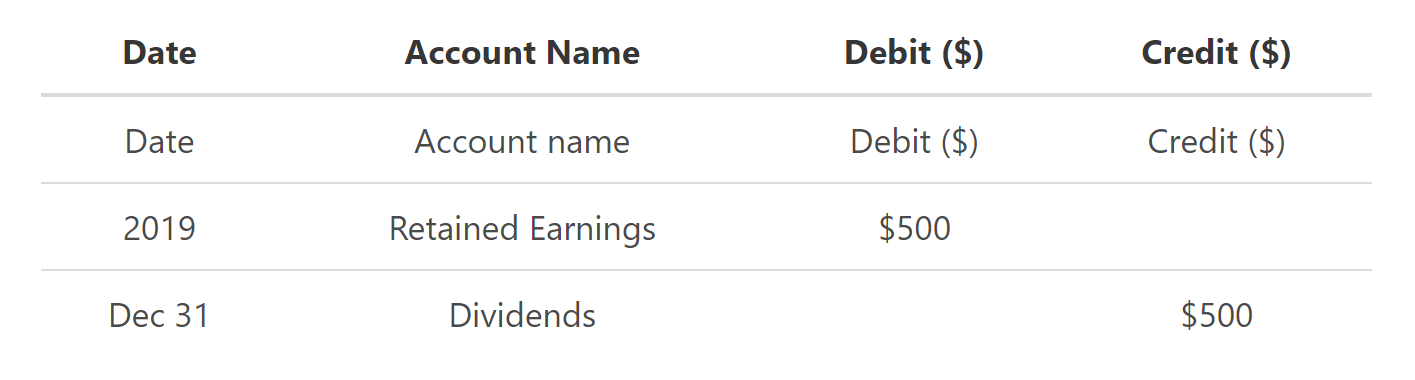

Closing Entry #4 for Bob

The last account to close is the dividend account. Here Bob needs to debit retained earnings account and credit dividends account.

Next Step

All of the temporary accounts have now been closed, and at this point the income summary account should have a balance which is equal to the net income shown on Bob’s income statement.

In the next tutorial, we’ll look at the income summary account in more detail.

FAQs

1. What is a closing entry?

A closing entry is an accounting entry that is used to transfer the balances of temporary accounts to permanent accounts. This is done as part of the annual financial closing process.

2. What are examples of closing entries?

Some common examples of closing entries include the closing of revenue accounts, expense accounts, and dividend accounts.

3. How is a closing entry recorded?

A closing entry is recorded by debiting the relevant temporary account and crediting the relevant permanent account.

4. What are the 4 closing entries?

There are four closing entries; closing revenues to income summary, closing expenses to income summary, closing income summary to retained earnings, and close dividends to retained earnings.

5. Which account is never closed?

Permanent accounts is never closed. This is because the balances of these accounts are transferred to the owner’s equity section of the balance sheet.

Permanent accounts are those that keep track of the long-term assets, liabilities, and equity of a business.