Reversing entries are journal entries that are made by an accountant at the beginning of the accounting cycle. This is an optional step in the accounting cycle and if the bookkeeper wishes can skip it entirely.

The purpose of these entries is to reverse the adjusting entries that were made in the previous financial reporting period. It is commonly used for revenue and expense account which had accruals or prepayments in the preceding accounting cycle and the accountant prefers not to keep these in the accounting system.

The Accounting Cycle Example

Throughout this series on the accounting cycle, we will look at an example business, Bob’s Donut Shoppe, Inc., to help understand the concepts of each part of the accounting cycle. Below is the complete list of accounting cycle tutorials:

- Journal Entries

- T-Accounts

- Unadjusted Trial Balance

- Adjusting Entries

- Adjusted Trial Balance

- Preparing Financial Statements

- Accounting Worksheet

- Closing Entries

- Income Summary Account

- Post-Closing Trial Balance

- Reversing Entries (you are here)

We also have an accompanying spreadsheet that shows you an example of each step.

Click here to download the Accounting Cycle template

When a reversing entry is not created, a bookkeeper/accountant needs to manually remember the adjusting entries from the last period and then account for these in the current period along with current periods revenues and expenses.

There are two key benefits to making a reversal entry:

- It significantly reduces the chances of making an error of double counting certain expenses or revenues.

- It will allow efficient processing of actual invoices during the current accounting period.

Why are Reversal Entries Needed?

Reversal entries will significantly make life of a bookkeeper easier since he won’t have to remember which expenses and revenues were accrued and prepaid. He can record the reversing entries to negate the effect of the adjusting entries that were passed in the preceding year and essentially start anew. For the current period, he would just have to record the expenses and revenue as they come in and not worry about the accrued and prepayments of the last period.

If the bookkeeper does not record these reversal entries, then he would have to remember which portion of the current expenses, for example, has already been paid out in the previous period. Therefore, there is a high chance of double-counting certain revenues and expenses. The practice of making reversal entries at the beginning of the accounting cycle will ensure that this error of double counting is avoided.

Since most bookkeeping is done using accounting software nowadays, this process is largely automated as well. While initially recording an adjusting entry in the previous period, the accountant would “flag” the entry. The accounting software will reverse this adjusting entry in the next accounting period so that the accountant does not have to remember to do this.

Examples of Reversing Entries

Let us take some examples of reversing entries to better understand the concept:

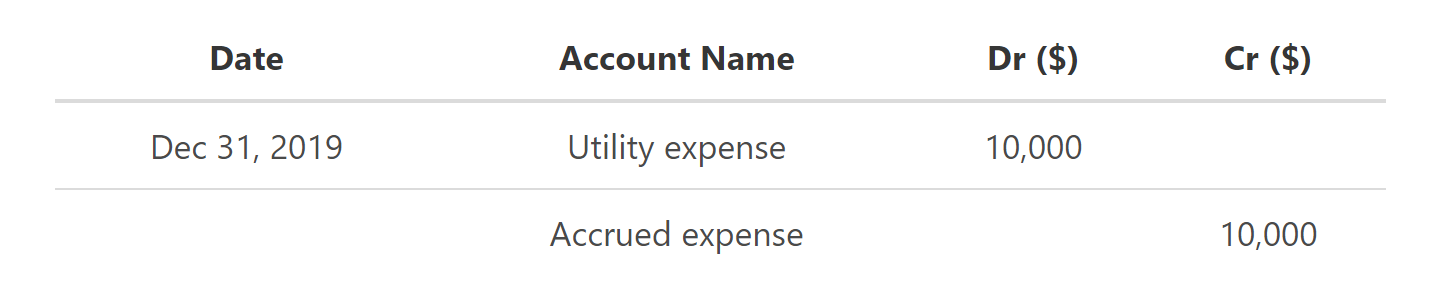

The following adjusting entry was made to record a Utility expense of $10,000 for the previous accounting period for which the invoice had not yet arrived and therefore not paid:

At the beginning of the new accounting period, this adjusting expense would have to be reversed. The reversal entry would create a negative amount of $10,000 in the expense account. Note that the expense accounts of the previous period have already been closed out to the retained earnings.

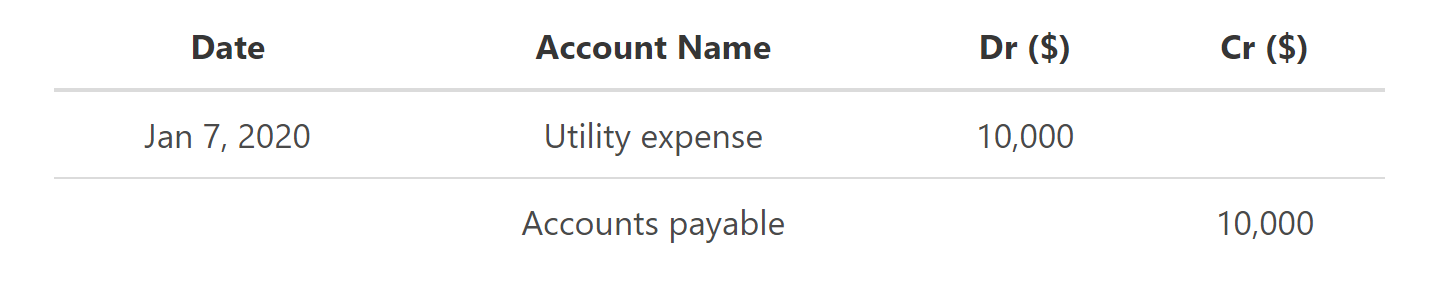

Now assume that the utility invoice arrives in the first week of January of this year. We will record the following entry:

This offsets the negative amount of the utility expense created at the beginning of January effectively meaning that the utility expense amount in the income statement for this period (January) becomes zero. Thanks to the reversing entry, the utility expense which relates to the previous period has been correctly recorded and there is no recognition for it in January accounts.

Reversing entries can also be created for:

- Accrued revenue. A company has earned $15,000 as it has delivered its service but has not billed its client yet. The adjusting entry made for it in the previous year was debit accrued revenue and credit revenue account. The reversing entry at the beginning of this year would be to debit revenue account and credit accounts receivable account. This would effectively create a negative amount of revenue at the beginning of this year. A few weeks into the current period, the customer is billed and so you record this by debiting accounts receivable and crediting revenue account.

- Prepaid expenses. A company prepays rent of $ 6,000 for January. The company accounts close in December. The adjusting entry recorded would be to debit prepaid rent and credit cash of $ 6,000. The reversal entry would be to debit cash and credit prepaid rent of $6,000. Once the rent is paid, the entry to record would be debit rent expense and credit prepaid rent of $6,000. Therefore, a rent expense of $6,000 is recorded for the current period in which it occurs.

- Unearned revenue. A company would be required to make adjusting entries and reversal entries to properly account for this type of transaction as well.

Bob’s Donut Shoppe, Inc. Example

The adjusting entries for Bob for the previous accounting period (January 2020) were:

To reverse these transactions and to create negative balances in the respective revenue and expense accounts, the following reversal entries need to be made:

The End of the Accounting Cycle

The reversal entries, although an optional step, marks the end of the accounting cycle. All of the steps will now need to be repeated and the process to be followed through again by the bookkeeper for the next accounting cycle.

FAQs

1. What is a reversing entry?

A reversing entry is an accounting entry that is made at the beginning of an accounting period to reverse the effects of a previous adjusting entry. The main purpose of a reversing entry is to ensure that the revenue and expense accounts are in balance. Generally, a company will only make reversing entries if it uses accrual basis accounting.

2. What is an example of a reversing entry?

An example of a reversing entry would be an accounting entry made to reverse the effects of a previous adjusting entry that was made for accrued revenue or prepaid expenses. A reversal entry would create a negative amount in the respective revenue and expense accounts. For accrual basis accounting, a company will only make reversing entries if it uses this method of accounting.

3. What is the difference between a closing and a reversing entry?

A closing entry marks the end of an accounting period and is used to transfer the balances in the revenue and expense accounts to the retained earnings account. A reversing entry is an accounting entry that is made at the beginning of an accounting period to reverse the effects of a previous adjusting entry. The main purpose of a reversing entry is to ensure that the revenue and expense accounts are in balance. Generally, a company will only make reversing entries if it uses accrual basis accounting.

4. What is the purpose of reversing entries in accounting?

The main purpose of reversing entries is to ensure that the revenue and expense accounts are in balance. Generally, a company will only make reversing entries if it uses accrual basis accounting. Without reversal entries, the balances in these accounts may not be accurate, which could lead to incorrect financial statements.

5. When are reversing entries used?

Reversing entries are generally used in accrual basis accounting. In this method of accounting, the reversing entries are used to ensure that the revenue and expense accounts are in balance. Without reversal entries, the balances in these accounts may not be accurate, which could lead to incorrect financial statements.